Deep Dive into the Rotary Wing Aircraft Rivets Market Segmentation

As the global demand for versatile and high-performance rotorcraft climbs, understanding the structural foundation of these machines becomes paramount. The rotary wing aircraft rivets market is not a monolithic industry; rather, it is a complex landscape defined by specialized components designed to survive the unique harmonic vibrations and structural loads of helicopters.

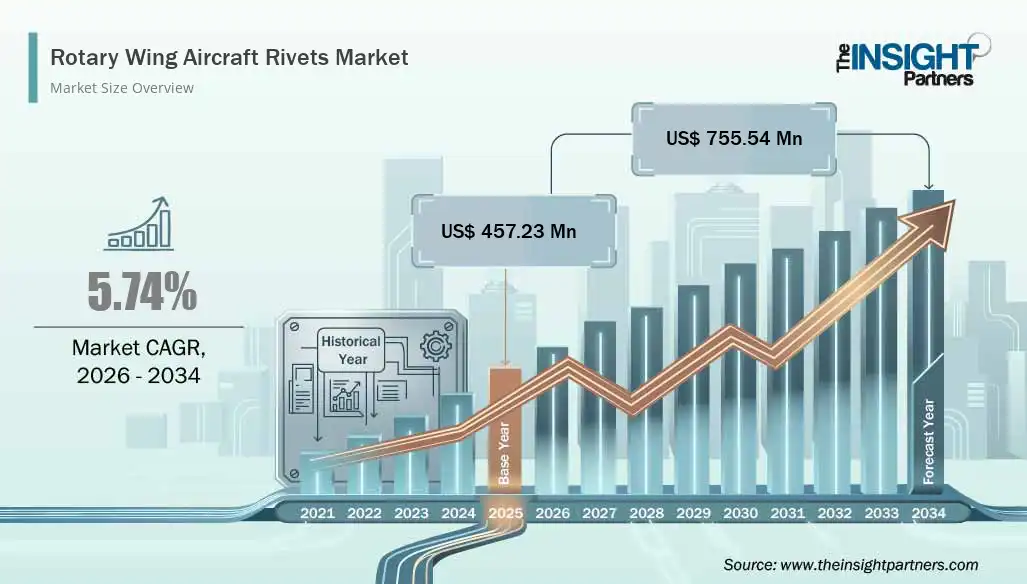

By the year 2034, this market is expected to reach a valuation of US$ 755.54 million, growing at a steady CAGR of 5.74 percent. To grasp how this growth is distributed, we must look closely at the primary segments Product Type, Material, and Application—that define the modern assembly line.

Download Sample Report –

https://www.theinsightpartners.com/Sample/TIPRE00018637

Market Segmentation by Product Type

The selection of a rivet type is dictated by the accessibility of the joint and the required load-bearing capacity. The market is primarily split into two dominant categories:

- Solid Rivets: These are the "gold standard" for helicopter airframes. Consisting of a solid shaft and a head, they require access to both sides of the structure for "bucking." Because they expand to fill the entire hole, they provide maximum vibration resistance—a critical factor for the longevity of rotary-wing platforms.

- Blind Rivets: Often referred to as "pop rivets," these are essential for components where only one side of the joint is accessible, such as internal electronics housings or closed tubular structures. Advancements in structural blind rivets are making them increasingly common in non-primary helicopter structures.

Market Segmentation by Material Type

Weight is the ultimate enemy of flight, and material science is the primary weapon against it. The rotary wing aircraft rivets market segments its materials based on the specific environment of the aircraft:

- Aluminum Alloys: Widely used for the general fuselage and skin panels due to their light weight and ease of installation. Alloys like 2117 and 2024 remain industry staples.

- Titanium Rivets: This is the fastest-growing material segment. Titanium is favored for its exceptional strength-to-weight ratio and its compatibility with composite materials. As more helicopters utilize carbon fiber, titanium rivets prevent the galvanic corrosion that occurs when aluminum meets carbon.

- Stainless Steel and Monel: These are reserved for high-temperature zones, such as firewalls and engine exhaust areas, where aluminum would lose its structural integrity.

Market Segmentation by Application

Where a rivet is placed determines the level of certification and precision required. The market is segmented into several key areas:

- Airframe Structures: This remains the largest segment, encompassing the fuselage, tail boom, and landing gear attachments. The sheer volume of fasteners required for a single airframe makes this a primary revenue driver.

- Flight Control Surfaces: Rivets used in rotors, rudders, and stabilizers must withstand extreme centrifugal forces and cyclic stress.

- Interior and Avionics: This segment utilizes smaller, often lighter fasteners to secure cockpit instrumentation and cabin linings.

The Role of End-Users: OEM vs. MRO

The market is further bifurcated by the stage of the aircraft's lifecycle. The Original Equipment Manufacturer (OEM) segment dominates the revenue share as new military and civil helicopter orders surge globally. However, the Maintenance, Repair, and Overhaul (MRO) segment is a vital secondary market. As existing fleets age, particularly in the defense sector, the replacement of fatigued or corroded rivets ensures that legacy aircraft remain airworthy and safe for continued service.

Contact Information -

Email: sales@theinsightpartners.com

Phone: +1-646-491-9876

Also Available in :