Why Is the Mobiltech Textiles Market Gaining Rapid Demand Globally? Which Regions Will Dominate the Mobiltech Textiles Market by 2034?

Global Mobiltech Textiles market was valued at USD 12.77 billion in 2025 and is projected to grow from USD 13.29 billion in 2026 to USD 16.63 billion by 2034, exhibiting a steady CAGR of 4.0% during the forecast period.

Mobiltech textiles are highly specialized, engineered materials developed specifically for the demanding requirements of automotive and mobility applications. These materials span a broad spectrum of functions—from interior seating fabrics and headliners that define cabin aesthetics and comfort, to mission-critical safety components such as airbags and seatbelt webbing, tire reinforcement cords, and multi-functional acoustic and thermal management nonwovens. What sets Mobiltech textiles apart from conventional textile materials is their engineered performance profile. They must simultaneously deliver occupant protection, contribute to vehicle lightweighting, reduce noise, vibration, and harshness (NVH), and comply with increasingly stringent environmental regulations covering flammability, volatile organic compound (VOC) emissions, and end-of-life recyclability. In a vehicle that must pass global safety standards while meeting ever-tighter emissions targets, these materials are far from peripheral—they are foundational to the vehicle's performance and compliance.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307001/mobiltech-textiles-market

Market Dynamics:

The market's trajectory is shaped by a complex interplay of powerful growth drivers, significant restraints that are being actively addressed, and vast, untapped opportunities that forward-thinking suppliers are already moving to capture.

Powerful Market Drivers Propelling Expansion

-

Rising Automotive Production and Vehicle Electrification Demands: The single most powerful driver of the Mobiltech Textiles market is the sustained growth in global vehicle production, particularly across emerging economies in Asia and South America where vehicle ownership rates continue to climb. However, it is the accelerating global transition to electric vehicles that is fundamentally reshaping demand patterns for automotive textiles. Because electric powertrains eliminate the masking noise of combustion engines, cabins become dramatically quieter—which means every rattle, wind noise, and road vibration becomes perceptible to occupants. This reality is forcing OEMs to invest significantly in advanced acoustic management textiles, including high-performance nonwovens and composite solutions designed specifically for NVH control. Furthermore, the thermal management requirements of battery electric vehicles create entirely new application areas for specialized textile materials, from battery compartment protection fabrics to lightweight insulation composites that help maintain optimal operating temperatures without adding excessive vehicle weight.

-

Stricter Global Safety Regulations Driving Restraint System Innovation: Regulatory bodies across North America, Europe, and increasingly Asia-Pacific are continuously raising the bar on occupant protection standards. The expansion of mandatory airbag requirements—from frontal airbags to side curtain, knee, and even pedestrian protection systems—is directly translating into higher volumes of technical airbag fabrics demanded per vehicle. Seatbelt webbing, while seemingly a mature product category, is also undergoing materials innovation to meet newer crash dynamics requirements and to integrate pre-tensioner technologies. These safety components are among the most technically demanding textile applications in the industry, subject to qualification cycles measured in years and auditing regimes that leave no margin for quality deviation. The result is a high-barrier, specification-driven segment that rewards established, technically capable suppliers and creates a durable competitive moat for market leaders.

-

Lightweighting Imperatives Creating New Material Opportunities: Whether driven by the fuel economy mandates governing internal combustion vehicles or the range optimization demands of electric platforms, automotive OEMs face relentless pressure to reduce vehicle mass. Every component is scrutinized, and textiles are no exception. The development of high-strength, low-weight textile constructions using advanced polyester, nylon, and aramid fibers—in applications ranging from tire reinforcement cords to structural composite preforms—is a direct response to this imperative. Suppliers who can demonstrate a credible weight reduction benefit while maintaining performance standards are consistently favored during platform sourcing decisions. This dynamic is accelerating R&D investment across the supply chain and encouraging the development of hybrid material solutions that combine textile and non-textile components into integrated, lightweight system modules.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307001/mobiltech-textiles-market

Significant Market Restraints Challenging Adoption

Despite robust underlying demand, the Mobiltech Textiles market faces a set of structural restraints that complicate growth and create friction across the value chain.

-

Raw Material Price Volatility and Supply Chain Fragility: Mobiltech textiles are heavily dependent on synthetic polymer fibers, primarily polyester and nylon, whose prices are linked to petrochemical feedstocks. Fluctuations in crude oil and chemical intermediate prices introduce meaningful cost uncertainty for textile manufacturers who operate under long-term fixed-price agreements with OEM customers. The ability to pass through raw material cost increases is limited in automotive supply chains, where price reduction expectations are deeply embedded in contract structures. This dynamic compresses margins and forces suppliers to absorb input cost volatility, creating financial stress particularly for mid-sized regional players who lack the procurement scale of global leaders. Furthermore, the COVID-19 pandemic exposed the structural vulnerabilities of globalized supply chains, and the automotive industry's experience with semiconductor shortages reinforced OEM awareness of single-source risk—prompting demands for supply chain diversification that add complexity and cost for textile suppliers.

-

Lengthy Certification and Qualification Processes for Safety-Critical Components: The path from material development to series production for safety-critical Mobiltech textiles is neither short nor straightforward. Airbag fabrics, seatbelt webbing, and tire reinforcement cords must pass through exhaustive qualification processes involving multiple rounds of physical testing, chemical analysis, and functional validation before receiving approval for use on a vehicle platform. These cycles can extend from 18 to 36 months and require substantial investment in testing infrastructure, documentation systems, and dedicated engineering resources. For new entrants or established players seeking to penetrate new safety segments, this represents a formidable barrier. Even approved materials face ongoing audit obligations and are subject to re-qualification if any process or material change is introduced, creating a persistent compliance burden that is proportionally heavier for smaller organizations.

Critical Market Challenges Requiring Innovation

The Mobiltech Textiles market faces a defining challenge at the intersection of sustainability and performance. Automotive OEMs have made increasingly ambitious public commitments to carbon neutrality, and those commitments extend across their supply chains—meaning textile suppliers are now being asked not just to deliver technical performance, but to demonstrate credible progress on recycled content integration, carbon footprint reduction, and end-of-life recyclability. The challenge is real: integrating post-consumer or post-industrial recycled polymers into safety-critical textiles without compromising the strength, consistency, and regulatory compliance of the finished material requires significant R&D investment and supply chain restructuring. Current certified recycled polymer capacity capable of meeting automotive technical specifications remains constrained, creating a bottleneck between OEM sustainability targets and supplier delivery capabilities.

Additionally, the industry is grappling with the growing complexity of multi-functional textile specifications. Where a seat fabric once needed to satisfy durability and aesthetics, it must now simultaneously address fogging and VOC emissions requirements, recycled content targets, flammability standards, and increasingly, bio-based content preferences—all at a cost point that is acceptable within competitive vehicle platform budgets. Managing this expanding specification matrix without sacrificing manufacturability or profitability is a challenge that demands continuous process innovation and close technical collaboration between material developers and OEM engineering teams.

Vast Market Opportunities on the Horizon

-

Advanced Acoustic and Thermal Management in Electric Vehicles: The global EV transition is not merely a disruption to existing demand patterns—it is generating entirely new application categories for Mobiltech textiles. The absence of combustion engine noise in EVs creates a qualitatively different acoustic environment inside the cabin, where road noise, wind noise, and even the sound of electrical systems become the dominant sources of occupant discomfort. Addressing these new acoustic signatures requires a new generation of nonwoven and composite textile solutions engineered specifically for the frequency profiles and spatial constraints of electric platforms. At the same time, battery thermal management demands are creating opportunities for specialized textile-based thermal interface materials and protective fabrics designed to perform reliably under the unique thermal cycling conditions of high-voltage battery systems. Suppliers who establish technical leadership in these emerging EV-specific applications are positioning themselves at the center of the industry's most consequential growth vector.

-

Sustainable Materials Innovation and Circular Economy Integration: The shift toward circular economy principles in the automotive sector is creating genuine commercial opportunities for Mobiltech textile suppliers who invest in sustainable material capabilities ahead of regulatory mandates. Regions with advanced circular economy policies—notably the EU, Japan, and California—are driving adoption of post-industrial and post-consumer recycled polyester in seating fabrics and headliners, with recycled content requirements projected to tighten further through 2030. Leading suppliers who develop traceable recycled polymer supply chains and qualify recycled-content materials against OEM specifications will enjoy a meaningful first-mover advantage in future sourcing competitions. Furthermore, bio-based fiber technologies, while still in earlier commercial stages for automotive applications, represent a longer-horizon opportunity that is attracting increasing R&D investment from both material innovators and OEM research programs.

-

Strategic Supply Chain Localization and Regional Capacity Expansion: The structural shift toward regional vehicle platform localization is creating compelling investment opportunities for Mobiltech textile suppliers with the capability and financial resources to establish manufacturing presence near new assembly hubs. Major Tier 1 suppliers increasingly require interior trim textile manufacturing within close proximity to final assembly plants, and OEMs are actively incentivizing supply chain localization through sourcing preferences in markets including Southeast Asia, Eastern Europe, and Mexico. This geographic realignment is driving announced capacity expansions and joint venture formations across multiple regions, creating opportunities for both global leaders to extend their footprint and for capable regional players to capture new business at the expense of distant suppliers unable to meet proximity and delivery requirements.

In-Depth Segment Analysis: Where is the Growth Concentrated?

By Type:

The Mobiltech Textiles market is segmented into Interior Trim Textiles, Safety Restraint Textiles, Tire Reinforcement Textiles, Acoustic & Thermal Nonwovens, and Underhood & Filtration Media. Interior Trim Textiles represent the broadest and most visible segment, directly shaping the passenger experience through cabin aesthetics, tactile quality, and comfort. However, their development trajectory is being fundamentally redirected by sustainability imperatives, lightweighting requirements, and tightening VOC and fogging standards. Safety Restraint Textiles—covering airbag fabrics and seatbelt webbing—remain the most technically demanding and highest-barrier segment, defined by non-negotiable performance standards, long qualification cycles, and uncompromising traceability requirements throughout the supply chain.

By Application:

Application segments include Seating & Interior Surfaces, Airbags & Seatbelts, Tires, Hoses & Belts, NVH Insulation & Filtration, and Carpets & Headliners. Seating & Interior Surfaces constitute the primary application volume, where innovation is focused on durability, ease of cleaning, premium tactile qualities, and responsible sourcing of materials. However, NVH Insulation & Filtration is rapidly gaining strategic importance as the defining growth application for the EV era. Electric vehicles require a fundamentally different approach to acoustic management and cabin air quality, creating strong demand for specialized nonwoven and composite textile solutions that deliver measurable performance improvements within tight weight and cost parameters.

By End-User:

The end-user landscape spans Automotive OEMs, Tier 1 System Integrators, and the Replacement & Aftermarket segment. Automotive OEMs are the dominant and most influential buyers in the market, exercising control over material specifications through platform-level sourcing programs that define standards for a vehicle's entire lifecycle. Their procurement model is characterized by long-term framework agreements, competitive bidding processes, and rigorous supplier qualification requirements. This creates a highly consolidated and specification-driven supply chain dynamic where the ability to achieve and maintain OEM qualification—and to execute that qualification consistently across global production sites—is the primary determinant of commercial success for textile suppliers.

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307001/mobiltech-textiles-market

Competitive Landscape:

The global Mobiltech Textiles market is moderately concentrated, with the top five suppliers controlling approximately 40% of total market revenue. This structure reflects the bifurcation between the highly technical, safety-critical segments—where global scale, deep OEM relationships, and extensive qualification histories create durable competitive advantages—and the more fragmented interior trim and acoustic management segments, where regional capabilities, design responsiveness, and just-in-time delivery performance are the key competitive differentiators. Market leadership in the safety-critical segments is firmly held by large-scale, vertically integrated multinationals such as Toray Industries (Japan), Kordsa (Turkey), and Hyosung Advanced Materials (South Korea), whose dominance is underwritten by their mastery of high-performance synthetic fiber technology, their global manufacturing footprints, and their long-standing OEM qualification histories. Alongside these global leaders, the market features strong regional specialists and focused component suppliers. The interior trim segment is served by players like Sage Automotive Interiors (U.S.), Seiren (Japan), and Aunde Group (Germany), while acoustic and thermal management segments are led by nonwovens specialists including Autoneum (Switzerland) and Freudenberg Performance Materials (Germany).

List of Key Mobiltech Textiles Companies Profiled:

-

Toray Industries (Japan)

-

Kordsa (Turkey)

-

Hyosung Advanced Materials (South Korea)

-

Teijin Frontier (Japan)

-

Autoneum (Switzerland)

-

Freudenberg Performance Materials (Germany)

-

Sage Automotive Interiors (U.S.)

-

Aunde Group (Germany)

-

Seiren (Japan)

-

SRF (India)

-

Kolon Industries (South Korea)

The competitive strategy across the market is overwhelmingly oriented toward R&D investment to advance material performance and accelerate sustainable material qualification, alongside forming deep, long-term technical partnerships with OEM customers and Tier 1 integrators to co-develop platform-specific solutions and secure future sourcing commitments well ahead of formal competitive tenders.

Regional Analysis: A Global Footprint with Distinct Leaders

-

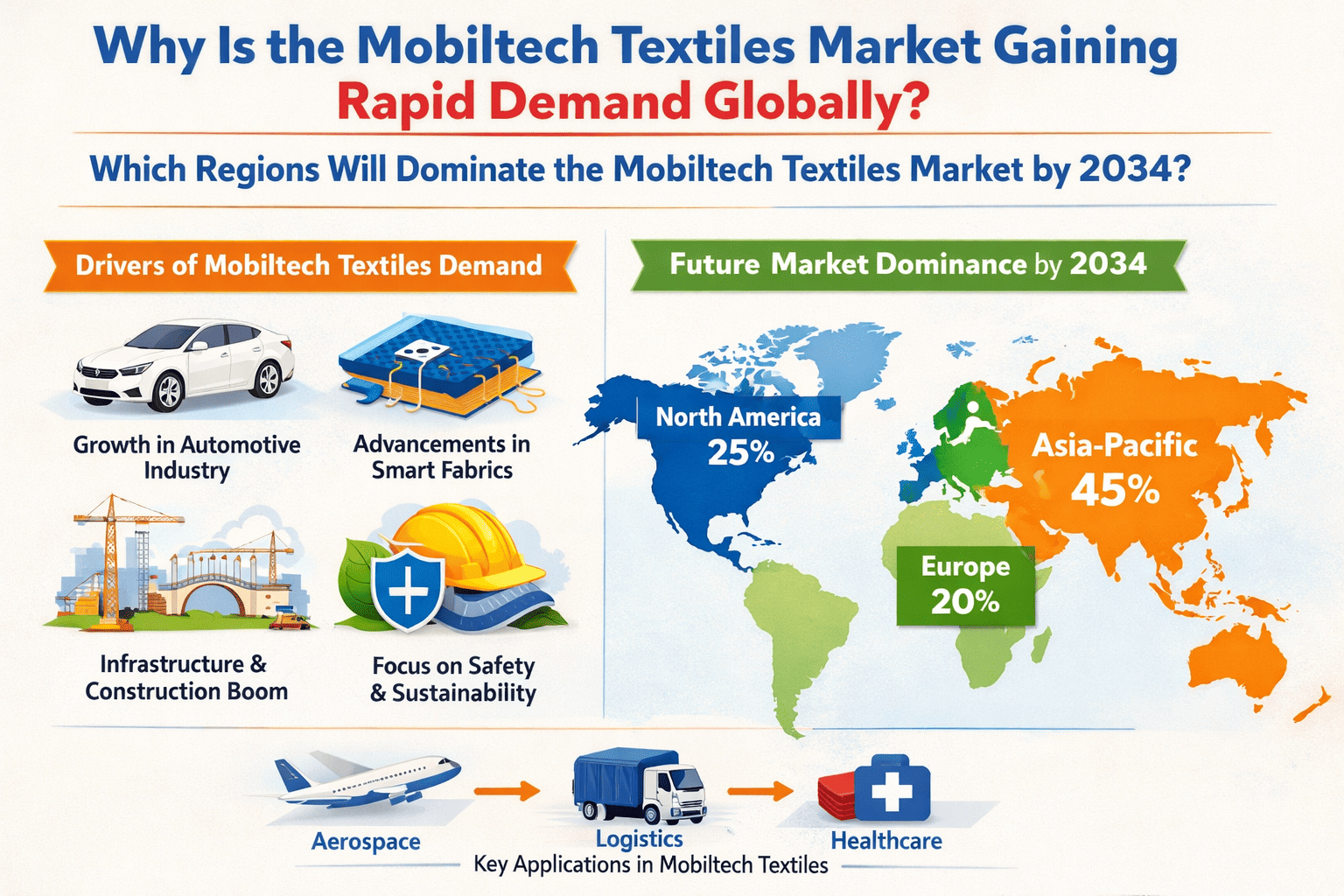

Asia: Is the undisputed center of gravity for the global Mobiltech Textiles market, anchored by China's position as the world's largest vehicle manufacturing hub. The region's unparalleled concentration of assembly plants generates immense, sustained demand for the full spectrum of automotive textile applications, from interior trim and safety restraints to tire reinforcement. The rapid adoption of electric vehicles across Chinese and wider Asian markets is further intensifying demand for advanced acoustic and thermal management textiles engineered specifically for EV platforms. Global suppliers have responded by establishing and expanding significant production capacity within the region to serve OEMs under just-in-time delivery models and to comply with local content requirements that are increasingly embedded in platform sourcing criteria.

-

North America & Europe: Together, these two regions form the established technology and premium segment leadership bloc for Mobiltech Textiles. North America is characterized by mature, technology-driven demand anchored by pick-up trucks, SUVs, and a rapidly growing premium EV segment, with procurement highly consolidated around long-term OEM framework agreements and stringent safety component qualification requirements. Europe, meanwhile, is defined by its sophisticated regulatory environment—encompassing EU vehicle safety standards, circular economy directives, and tightening CO2 fleet targets—that collectively make it the global trendsetter for sustainable interior materials, low-emission textile chemistries, and the integration of recycled content across automotive textile applications. Both regions continue to attract significant supplier investment in advanced nonwoven and composite capabilities.

-

South America and Middle East & Africa: These regions represent the emerging frontier of the Mobiltech Textiles market. While currently smaller in scale, they are characterized by regional assembly operations, growing vehicle ownership, and progressive supply chain localization by global OEMs seeking to serve these markets more efficiently. Demand is presently weighted toward interior trim, carpet, and basic nonwoven applications, with cost-effective durability being the primary procurement criterion. However, as platform localization deepens and OEM technical requirements migrate to these markets, both regions present meaningful long-term growth opportunities for suppliers with the capability to establish credible regional manufacturing and qualification capabilities.

Get Full Report Here: https://www.24chemicalresearch.com/reports/307001/mobiltech-textiles-market

Download FREE Sample Report: https://www.24chemicalresearch.com/download-sample/307001/mobiltech-textiles-market

About 24chemicalresearch

Founded in 2015, 24chemicalresearch has rapidly established itself as a leader in chemical market intelligence, serving clients including over 30 Fortune 500 companies. We provide data-driven insights through rigorous research methodologies, addressing key industry factors such as government policy, emerging technologies, and competitive landscapes.

-

Plant-level capacity tracking

-

Real-time price monitoring

-

Techno-economic feasibility studies

International: +1(332) 2424 294 | Asia: +91 9169162030

Website: https://www.24chemicalresearch.com/